Why a Recession May Be Coming: What the Yield Curve and Historical Data Tell Us

In this blog post, we delve into how historical patterns and market behavior provide crucial lessons for understanding economic cycles, with a focus on the yield curve as a recession predictor. By examining past recessions, Federal Reserve actions, and the natural reversion of the yield curve, we uncover consistent signals of economic downturns. The post draws on historical data and well-documented trends to emphasize the importance of learning from the past to better anticipate and prepare for future challenges.

ECONOMIC EVENTSMARKET DYNAMICSFINANCIAL ANALYSISFINANCIAL MARKETSINVESTMENT ANALYSISMARKET ANALYSISECONOMIC CONDITIONSRISK MANAGEMENTMARKET VOLATILITYTECHNICAL ANALYSISRECESSIONMARKET TRENDS

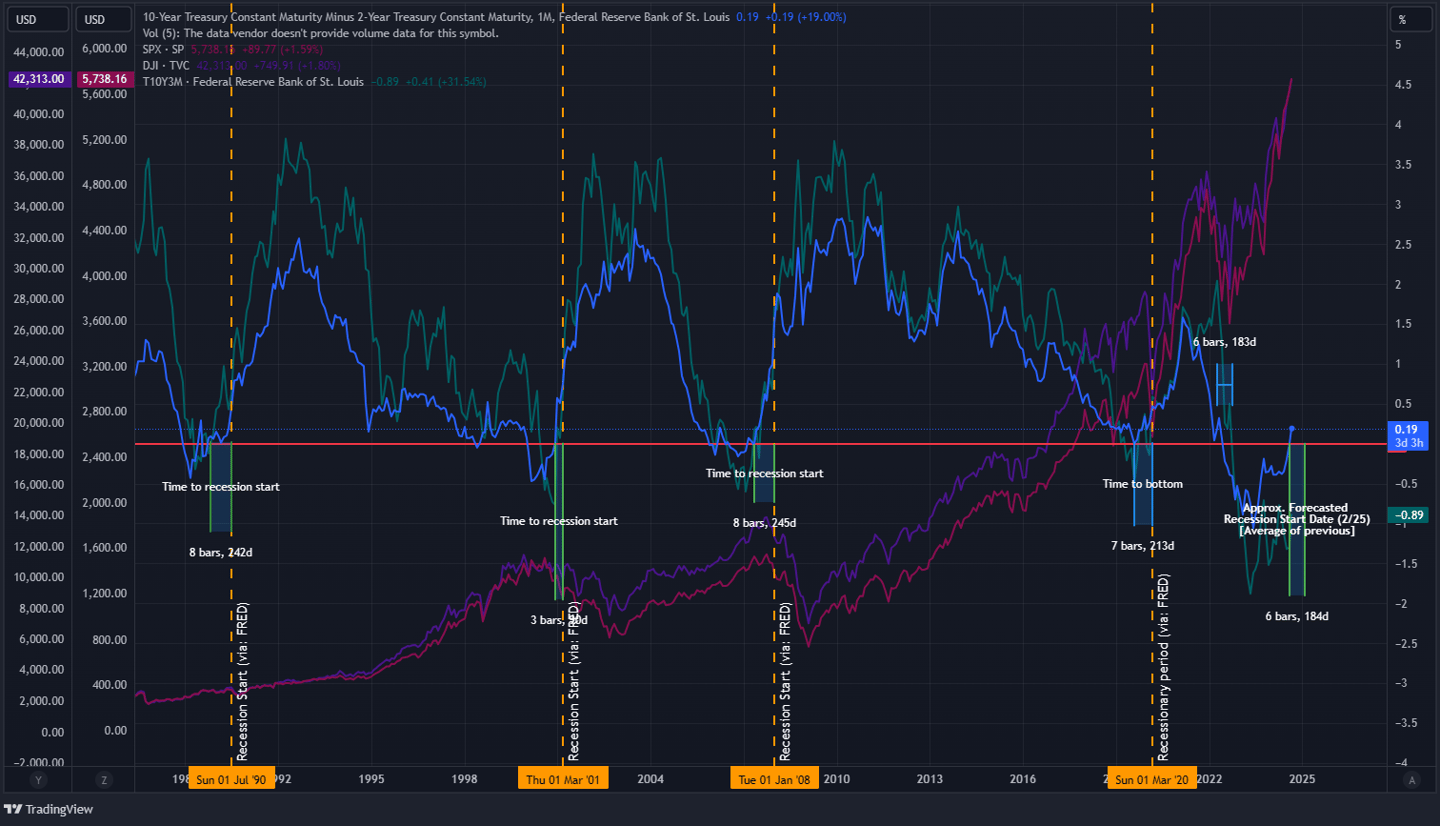

As we move toward 2025, market watchers and economists are increasingly concerned about a potential recession looming in the next 12-18 months. One of the most reliable predictors of an economic downturn—the inverted yield curve—has been signaling trouble for quite some time. However, there’s another important signal that deserves attention: the reversion of the yield curve to its normal shape. Historically, this shift back to an upward slope has often coincided with the onset of recessions. While some argue that Federal Reserve actions trigger these shifts, others suggest the Fed is merely responding to natural economic cycles already in motion.

What is the Yield Curve?

The yield curve shows the relationship between interest rates on short-term and long-term government bonds. Typically, long-term bonds yield higher interest because they require a longer commitment. But when short-term rates exceed long-term rates, the curve inverts, signaling that investors expect an economic slowdown.

While much attention is given to the inversion of the yield curve as an early recession signal, the reversion to a normal upward slope may be even more significant, as it often marks the point when economic deterioration becomes undeniable.

Why the Yield Curve Reverts to Normal

The reversion of the yield curve is a complex phenomenon. On the surface, it may appear that the Federal Reserve’s actions—such as rate cuts—are the primary cause of this normalization. However, a deeper analysis suggests that the Fed is reacting to existing economic conditions rather than creating them. Here’s why:

Natural Economic Cycles: The economy operates in cycles of expansion and contraction. When growth slows and risks of a downturn emerge, market forces push investors toward long-term bonds, stabilizing their yields. Simultaneously, weakening economic activity naturally reduces demand for short-term borrowing, leading to a decline in short-term rates.

Market Behavior Precedes Policy: Often, the yield curve begins reverting before the Federal Reserve takes action. This timing suggests that the reversion reflects market expectations of slowing economic growth and future monetary easing, not the direct result of Fed intervention.

Fed’s Reactionary Role: By the time the Federal Reserve cuts rates, the yield curve’s reversion is usually already underway. This sequence implies the Fed is responding to economic signals rather than driving them, acting as a stabilizing force rather than a catalyst.

Historical Precedents: Yield Curve Normalization, Fed Actions, and Recessions

The relationship between yield curve normalization, Federal Reserve actions, and recessions offers valuable insights into economic cycles. Historical data reveals that the Federal Reserve’s first rate cuts after a yield curve normalization often align closely with the onset of a recession. Here are three key examples:

2008 Financial Crisis:

Yield Curve Inversion: The yield curve inverted on December 27, 2005, when the 10-year Treasury yield dropped below the 2-year yield, signaling early market concerns about long-term economic stability.

Yield Curve Normalization: The curve reverted to its normal upward slope in June 2007, as the 10-year yield surpassed the 2-year yield. This reversion reflected market expectations of an impending economic slowdown.

Federal Reserve’s First Rate Cut: Following the normalization, the Fed made its first rate cut on September 18, 2007, lowering the federal funds rate by 50 basis points. This marked the beginning of aggressive monetary easing to address growing economic pressures.

Recession Onset: The Great Recession officially began in December 2007, just three months after the Fed’s first rate cut, underscoring the reversion as a precursor to economic contraction.

2001 Dot-com Bust:

Yield Curve Inversion: The curve inverted on February 2, 2000, as the 10-year Treasury yield fell below the 2-year yield amid overvalued tech stocks and slowing corporate investment.

Yield Curve Normalization: By December 2000, the curve had returned to its normal slope, signaling growing concerns about the economy’s ability to sustain growth.

Federal Reserve’s First Rate Cut: On January 3, 2001, just one month after the yield curve normalized, the Fed cut rates by 50 basis points to mitigate the fallout from the collapsing tech bubble.

Recession Onset: The recession officially began in March 2001, two months after the first rate cut, illustrating how normalization and rate cuts often align with imminent downturns.

Early 1990s Recession:

Yield Curve Inversion: The yield curve inverted on December 13, 1988, when short-term borrowing costs exceeded long-term returns, reflecting market concerns about overheating.

Yield Curve Normalization: The curve returned to a normal slope in May 1989, as economic activity began to show signs of weakness.

Federal Reserve’s First Rate Cut: The Fed responded with its first rate cut on June 6, 1989, just one month after the curve normalized, to address growing economic concerns.

Recession Onset: The recession began in July 1990, approximately 13 months after the Fed’s first rate cut, highlighting the delayed impact of economic adjustments.

These examples highlight a consistent sequence:

Inversions act as early warnings, indicating long-term concerns about economic stability.

Normalizations occur as markets respond to weakening growth, signaling a shift in economic conditions.

Fed rate cuts follow normalization, aligning with worsening economic indicators and often preceding the formal onset of a recession.

By examining these precedents, we see how the yield curve’s normalization, combined with the timing of Federal Reserve interventions, provides a critical window into the dynamics of economic downturns. This understanding reinforces the yield curve’s role as a key predictor of recessions.

The Current Situation: Reversion and Fed Action in 2024

The yield curve reverted to its normal upward slope on September 6, 2024, after over two years of inversion—a record duration. This reversion occurred just days before the Federal Reserve announced its first rate cut of the year on September 18, 2024, lowering the federal funds rate by 50 basis points (Advisor Perspectives)

While the Fed’s rate cut may seem like the catalyst for the reversion, evidence suggests otherwise:

The curve began reverting before the rate cut, signaling that market forces were already shifting in anticipation of a slowdown.

Investor expectations drove the change, as markets began pricing in future Fed actions and adjusting to a weaker economic outlook.

This timeline underscores the hypothesis that the Federal Reserve is reacting to cyclical economic forces, not initiating them.

If history is any guide, the current reversion could signal a recession as soon as February 2025, as indicated by the timeline shown in the chart above.

Why This Matters

Understanding the yield curve’s reversion as a natural part of economic cycles rather than a direct result of policy changes shifts the focus to the broader market dynamics at play. It highlights that:

Reversions are a late-stage signal of economic weakness, often marking the final phase before a recession.

The Fed’s role is reactionary, aiming to stabilize rather than dictate economic outcomes.

Market forces lead the way, with investor behavior reflecting underlying economic realities.

The Takeaway

While inverted yield curves serve as early warnings, their reversion to a normal slope is an even more critical signal that a recession may be imminent. This reversion is not simply a result of Federal Reserve actions but rather a natural outcome of market adjustments to economic slowdowns. The Fed’s rate cuts may amplify or accelerate these changes, but they do not cause them.

As we look ahead to 2025, the reversion of the yield curve reminds us that the economy operates on cycles driven by market forces, investor sentiment, and underlying economic conditions. While the Federal Reserve plays a critical role in responding to these changes, its actions are reactive, aiming to mitigate damage rather than dictate outcomes.

What Does This Mean for the Economy?

The yield curve’s reversion, coupled with the Federal Reserve’s recent rate cuts, suggests that the economy may already be at a tipping point. Historically, recessions have followed soon after yield curve normalizations, as economic activity slows and market sentiment shifts. Businesses, investors, and individuals should prepare for these potential outcomes:

For Businesses: Focus on operational efficiency and risk management. Consider strategies to weather slower demand and tighter financial conditions.

For Investors: Prioritize safer assets and diversify portfolios to reduce exposure to volatile sectors. Monitor long-term bonds, which often outperform during recessions.

For Individuals: Build emergency savings and limit discretionary spending to prepare for potential economic challenges such as job market instability.

Final Thoughts

The yield curve’s reversion to a normal slope is more than a technical adjustment—it’s a profound indicator of the economy’s transition into a slower growth phase. By understanding this shift as part of natural economic cycles, we gain valuable insights into what lies ahead and how to prepare.

While Federal Reserve actions often draw the spotlight, they are better understood as responses to market-driven dynamics rather than the drivers of change. As the economy heads into 2025, the yield curve’s message is clear: a recession may no longer be a distant possibility but an imminent reality.

By staying informed and proactive, we can better navigate the challenges of these economic cycles and position ourselves for stability and resilience.

Disclaimer:

The information provided in this article is for informational purposes only and should not be considered financial advice. Always perform your own due diligence before making any investment decisions.

"The longer you can look back, the farther you can look forward"

– Winston Churchill, March 1944